Navigating Energy Markets: Who Are the Main Players?

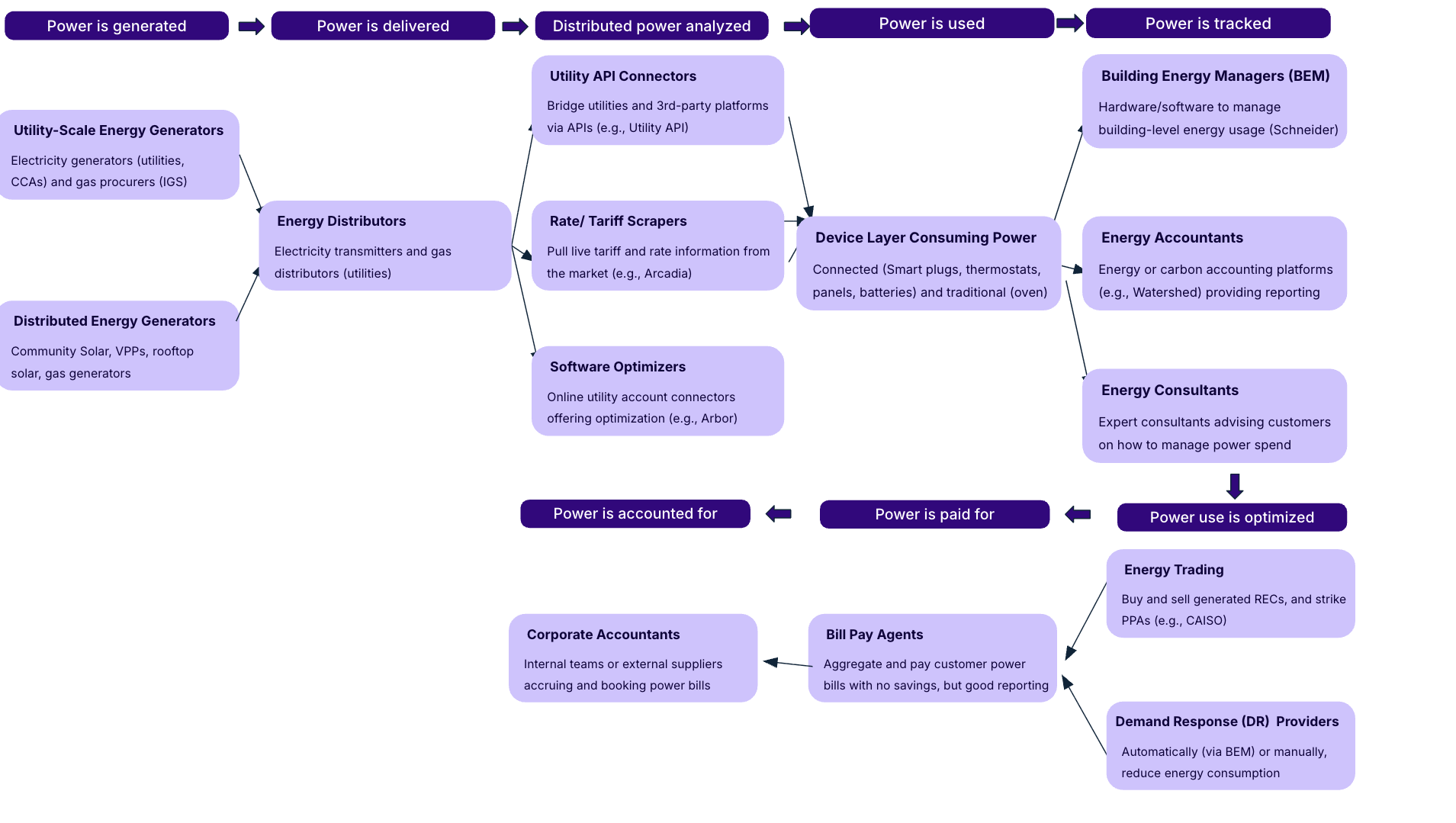

For most businesses, utility bills arrive as a single monthly line item—opaque, unpredictable, and often frustrating. But behind every invoice is a vast network of players, each capturing a piece of value as energy is generated, delivered, optimized, and ultimately paid for. For CFOs and finance leaders, understanding this landscape is essential. Energy costs often rank as a top-three non-payroll operating expense, and the choices made in navigating this system can mean millions in savings—or millions left on the table. Broadly speaking, the energy market can be divided into two domains: Front of the meter: how electricity and gas are generated and delivered to a building’s meter. Behind the meter: how energy use is tracked, optimized, and ultimately paid for inside the building.

Front of the Meter: From Generation to Delivery

The “front of the meter” describes the supply chain that brings electrons from power plants, solar farms, or gas fields to the utility meter on your property. It includes four major archetypes:

1. Power Generators

- Who they are: Utilities, community choice aggregators (CCAs), community solar developers, and natural gas procurers.

- What they do:

- Utilities own or contract with large-scale generation assets and sell electricity at regulated or semi-regulated prices.

- CCAs buy energy in bulk on behalf of communities, often at better rates or with higher renewable content.

- Community solar developers build shared projects where multiple businesses or households can subscribe to a slice of the output.

- Gas procurers source natural gas cheaply in wholesale markets and resell it at a margin.

- Utilities own or contract with large-scale generation assets and sell electricity at regulated or semi-regulated prices.

- Key context for CFOs: Generators are the ultimate origin of costs. Their pricing fluctuates with market conditions, regulations, and infrastructure investment cycles.

2. Power Deliverers

- Who they are: Primarily regulated utilities.

- What they do: Manage the transmission and distribution system—moving power from generators to end customers. They maintain the poles, wires, transformers, and substations that keep electricity flowing.

- How they charge: Delivery costs are typically fixed or usage-based fees on top of generation charges.

- Key context for CFOs: Even if you shop for cheaper generation, delivery fees are usually unavoidable. These costs are regulated but can still shift over time as utilities invest in infrastructure.

3. Analysis Layer

- Who they are: API providers, rate and tariff databases, and third-party software optimizers.

- What they do: Provide access to utility data, scrape rate schedules, and create tools that help compare costs across markets and tariffs.

- Key context for CFOs: These intermediaries exist because utility billing structures are highly fragmented. Accurate data is crucial for cost control, but quality varies widely depending on the provider.

4. Power Consumers (Device Layer)

- Who they are: Connected hardware providers such as smart thermostat manufacturers, battery companies, and panel-integrated monitoring devices.

- What they do: Enable more granular control over energy consumption through hardware and IoT connectivity.

- Key context for CFOs: These devices can help reduce demand charges or shift usage to off-peak times, but adoption often requires upfront capital and long-term ROI analysis.

Behind the Meter: From Usage to Payment

Once power crosses the building’s meter, it enters the “behind the meter” landscape—where businesses decide how to use, track, optimize, and pay for it.

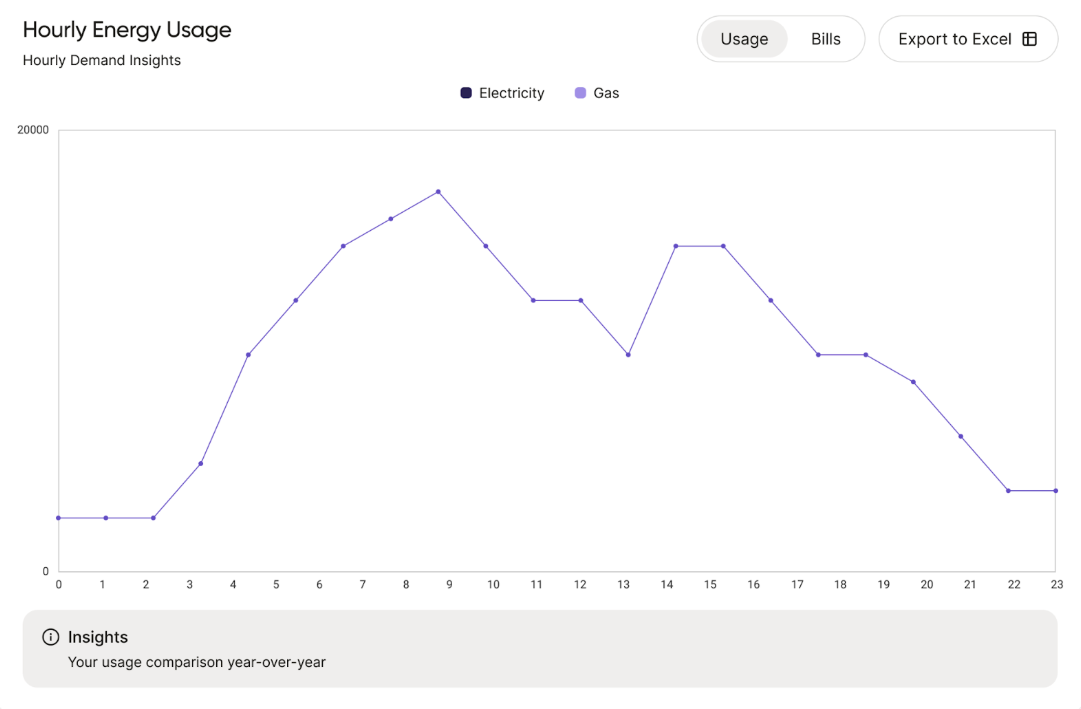

1. Power Tracking

- Who they are: Building energy management (BEM) providers, load management systems, IoT platforms, and smart devices.

- What they do: Provide visibility into how and when energy is being consumed, often integrating sensors, submeters, and analytics platforms.

- Key context for CFOs: These systems are valuable for operational teams, but their impact depends on whether insights translate into actual cost savings.

2. Energy Marketplaces

- Who they are: Independent system operators (ISOs), wholesale markets, and demand response platforms.

- What they do: Facilitate trading of electricity supply, renewable energy credits (RECs), and grid services. Businesses can sometimes participate directly through brokers or aggregators.

- Key context for CFOs: Accessing these markets can unlock savings but requires sophistication. Most businesses rely on intermediaries to capture value.

3. Power Payments

- Who they are: Bill pay agents and utility payment processors (e.g., Capturis, Engie).

- What they do: Aggregate bills across multiple sites, process payments, and provide consolidated reporting.

- Key context for CFOs: These services reduce administrative burden but add cost. Importantly, they rarely deliver savings—they simply streamline payment.

Why This Matters for Finance Leaders

Every player in the energy market takes a cut. Some add true value—through cheaper supply, operational efficiency, or better transparency. Others simply move money around.

For CFOs of multi-location businesses, the challenge is not only understanding who the players are, but also separating value-adding partners from administrative pass-throughs. By mapping the front- and behind-the-meter ecosystems, finance leaders gain the context needed to ask the right questions, identify hidden costs, and build a more predictable approach to energy spend.

👉 Next time you look at a utility invoice, remember: it isn’t just one bill. It’s the sum of decisions and charges made by dozens of stakeholders across the market. The more you understand their roles, the better equipped you’ll be to control one of your largest and least predictable expenses.

Resources

Learn more about energy savings

Stay up to date with our latest publications.